The COVID-19 pandemic and subsequent stay-at-home orders saw a boom in all things remote—education, work, dating, and of course, medicine. A massive new deal has come as a result of that explosive growth, one that could create a new standard in global healthcare’s delivery, access, and experience.

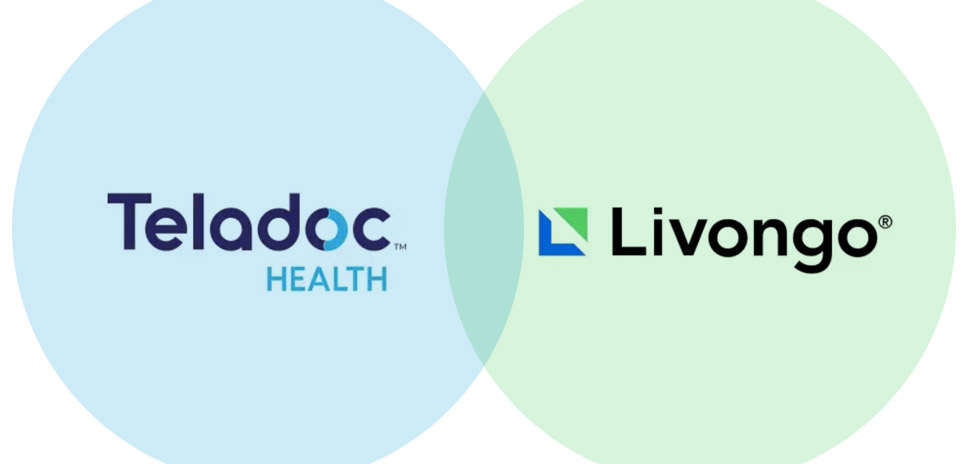

North Texas-founded Teladoc Health, one of the nation’s largest telemedicine providers, has entered into a definitive merger agreement with Linvongo, which has developed tech to help monitor and manage patients’ chronic conditions like diabetes.

Per Forbes, Teladoc has agreed to purchase Livongo for $18.5 billion, creating a $38 billion entity. The deal represents the combination of two of the largest publicly traded virtual care companies, which makes for “the market’s first full-stack virtual health company.”

Teladoc said in its announcement that together with Livongo, a global leader in consumer centered virtual care will emerge.

The Associated Press defines telemedicine as “care delivered remotely, often with a live video connection through patient smartphones or tablets.” The pandemic caused millions to try it earlier this year, in everything from routine care to specialist appointments.

Researchers predict that telemedicine, though it was initially slow to catch on, could play a greater role in healthcare even after the COVID-19 pandemic has died down. “That’s partly because people have become more used to it, and they may be more wary now of sitting in waiting rooms filled with other sick patients,” AP notes.

Before that, AP said that health insurers should decide whether to make “some pandemic-driven coverage expansions of telemedicine permanent.” Also, how much should be paid for it.

Teladoc was founded in Lewisville in 2002 before moving to Purchase, New York. That makes it one of the oldest telemedicine companies in the country. (We briefly explored its history in 2016.)

But the company has expanded tremendously since then. Teladoc said its total visits in the second quarter tripled to 2.8 million and revenue grew by 85 percent.

In Teladoc’s announcement, CEO Jason Gorevic—who will be CEO of the combined company—called Livongo a world-class innovator with demonstrated success that Teladoc deeply admires. The two companies are complementary and plan to combine services to create substantial value in the industry.

That means together “enabling clients everywhere to offer high quality, personalized, technology-enabled longitudinal care that improves outcomes and lowers costs across the full spectrum of health.”

The merger is a transformational opportunity for the two companies to improve how consumers get healthcare across the globe.

“This merger firmly establishes Teladoc Health at the forefront of the next-generation of healthcare,” he said. “Together, we will further transform the healthcare experience from preventive care to the most complex cases, bringing ‘whole person’ health to consumers and greater value to our clients and shareholders as a result.”

Glen Tullman, founder and executive chairman of Livongo, called the combination highly strategic. He expects the new company to be a leader in consumer-centered virtual care. He also said the merger will provide an opportunity for Livongo to further accelerate the growth of its data-driven member platform and experience.

“By expanding the reach of Livongo’s pioneering Applied Health Signals platform and building on Teladoc Health’s end-to-end virtual care platform, we’ll empower more people to live better and healthier lives,” he said in a statement. “This transaction recognizes Livongo’s significant progress and will enable Livongo shareholders to benefit from long-term upside as the combined company is positioned to serve an even larger addressable market with a truly unmatched offering.”

According to CNBC, the deal came together in less than three months, despite the coronavirus pandemic forcing a lockdown across the country. Getting it done was a “major logistical challenge” given the circumstances, but the “two companies had been talking about a partnership for years.”

“Our two companies were either on a path of convergence or collision,” Gorevic told CNBC.

![]()

Get on the list.

Dallas Innovates, every day.

Sign up to keep your eye on what’s new and next in Dallas-Fort Worth, every day.

R E A D N E X T

-

Dallas-based MyndVR, a leading provider of virtual reality solutions for seniors and “active agers,” has partnered with Healing HealthCare Systems to offer Continuous Ambient Relaxation Environment VRx (C.A.R.E.) to residents who use the MyndVR system at senior and memory care communities, assisted living centers, hospice care, and in the home. Using gaze-based navigation with VR headsets, users can interact with the immersive C.A.R.E. VRx app, which blends voice-based, guided imagery with 360-degree visuals of forests, lakes, beaches, and more.

-

Put your problem-solving chops to work. The Children's Health event encourages gamification, augmented reality to solve for age-old pediatric health care problems. There's even a no-code challenge.

-

Women entrepreneurs—especially those in the tech world—have something to keep them warm at home Thursday during tomorrow's winter storm: The DEC Network’s inaugural, all-virtual Women X Tech event, from 11 a.m. to 4:30 p.m., is designed to help women founders from all tech industries connect, learn, and grow their businesses.

-

The award from the National Institutes of Health will help HSC lead the AI/Machine Learning Consortium to Advance Health Equity and Researcher Diversity, or AIM-AHEAD, program. The effort will bring together experts in community engagement, AI/ML, health equity research, data science training, and data infrastructure.

-

The pop-up digital showroom is a 360-degree, 3D beauty experience